The LPI, the NFT and the TLAs

Linux Professional Institute (LPI) regularly hosts students and other folks with an interest in a career involving open source. Through internships, we help them gain experience and acquire new skills. In return, we get to introduce (or further expose) these interns to the world of open source software.

This summer, in Canada, we have two students; Alex, who is studying communications and PR, and Rozilyn, who is studying electrical and computer engineering. During a call earlier this summer, the conversation turned into a search for a project that would interest the interns and benefit the open source community.

We quickly settled on the subjects of cryptocurrencies along with the current mania over non-fungible tokens (NFTs). The case was made that launching new coins, tokens, or other crypto-assets such as NFTs is now relatively easy, technically speaking, and worth demonstrating in order to demystify the process.

Looking for inspiration, we discussed creating an NFT of each version of LPI’s certification objectives since 1999 (similar to Tim Berners-Lee’s “Source Code for WWW” NFT), or an open source counterpart to the cleverly generated CryptoPunks icons and NFTs.

Considering the general interest in crypto-related topics – and, I suppose, because one of the interns’ fields of study was communications – Alex and Rozilyn decided to share their project and progress with us in a series of blog postings. I’m certain you will enjoy reading what they learn this summer, as well as what they end up creating.

So without further ado, here’s the first check-in from Alex and Rozilyn:

A Brief History of Cryptocurrency

Cryptocurrency (or “crypto” for short) requires no regulation from a bank or government. Instead, cryptocurrency is managed by software using cryptographic math. Crypto payments are digitally tracked and verified through a financial ledger, now commonly referred to as a “blockchain.”

Though a seemingly recent phenomenon, cryptocurrency was first proposed by American cryptographer David Chaum in 1983, 10 years prior to CERN’s release of the World Wide Web for public use. “Digital asset software” now exists in the thousands, in forms such as Ethereum, Litecoin, and Dogecoin.

DigiCash, the fruition of Chaum’s ideas, became the first cryptocurrency in 1995. In 1997, the same verification systems that would later appear in modern software such as Bitcoin or Ethereum were used for “Bit gold,” a proposal by computer scientist Nick Szabo.

No cryptocurrencies followed DigiCash until the catastrophic market crash of 2008. Dwindling faith in the financial reliability of banks and government—along with their standard currencies, known as fiat currencies—created an urge for decentralized solutions. One year later, an alternative now known as Bitcoin emerged as open source software.

Bitcoin was published under the pseudonym “Satoshi Nakamoto” in documentation known as the “white paper”. Some suspect a connection to the original Szabo, who has denied the claims. Today, Bitcoin, along with its crypto-counterparts, is a popular alternative to fiat currencies for those seeking a currency controlled by people, not institutions—and of course, to use when purchasing NFTs.

How Cryptocurrency Works:

A financial ledger is a history of money paid or owed by a group. In cryptocurrency, payments are recorded in a digital ledger, also known as a blockchain, and secured through a digital signature. These digital signatures are uniquely produced with each transaction to maintain the security of a person’s digital “‘wallet,” which stores crypto-coins.

How much crypto an individual owns (or spends) is confirmed through the blockchain. A transaction is verified by software that retrieves the full history of transactions of that currency up until the transaction. This explanation is a technical simplification, and we invite you to view a more comprehensive video about Bitcoin. But in essence, the history of transactions, or the ledger, replaces the need for physical representations of currency.

Ethereum and NFTs

A non-fungible token (NFT) is a digital file—typically a photo, video, or audio recording—that represents a transaction on the blockchain. “Fungible” means something exchangeable, such as a dollar bill that can be switched for any other dollar bill without any effect on its meaning or value. Therefore, “non-fungible” refers to an object such as a painting that is unique and irreplaceable.

The twist: NFTs are often valued at millions of USD. The most valuable NFT was priced at $69 million dollars.

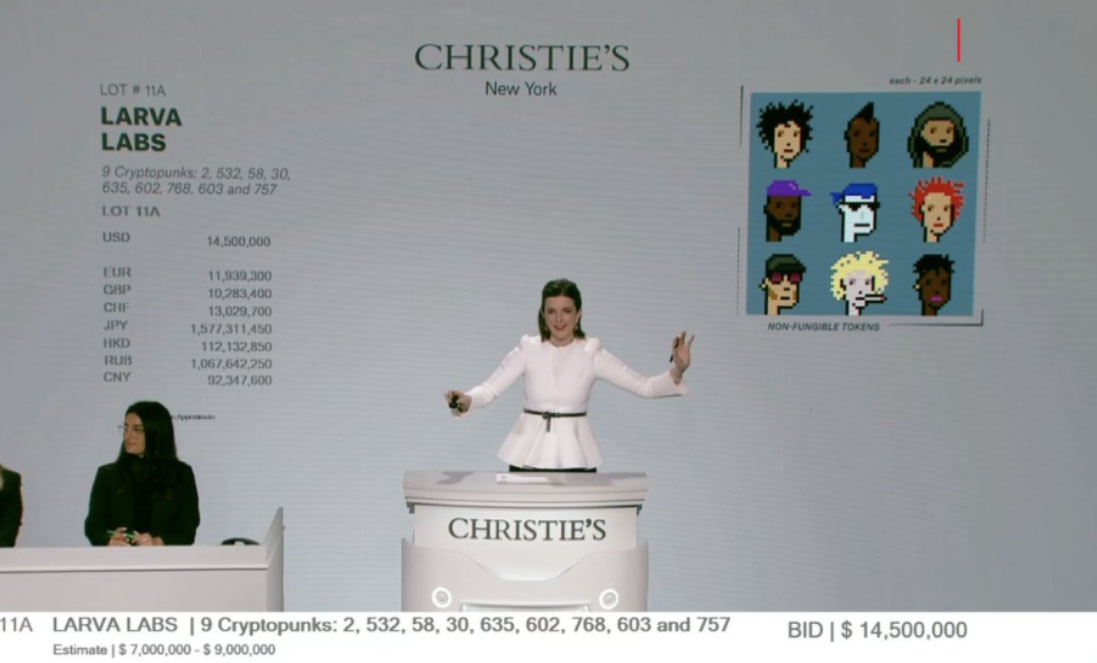

NFTs were first created using the cryptocurrency Ethereum in 2015, entering popular culture two years later with the release of CryptoPunks: 10,000 algorithmically generated punk characters, each of which was 50 x 50 pixels in size and reached a sale price as high as $16.96 million USD for a set of nine (Figure 1).

Figure 1: One of the earliest NFT projects, CryptoPunks, auctioned as a seven-token set at Christie’s for $17 000 000 USD.

CryptoPunk NFTs were coded using ERC-721, which would become the first standardized “smart contract,” a program that manages transactions and stores them on the blockchain.

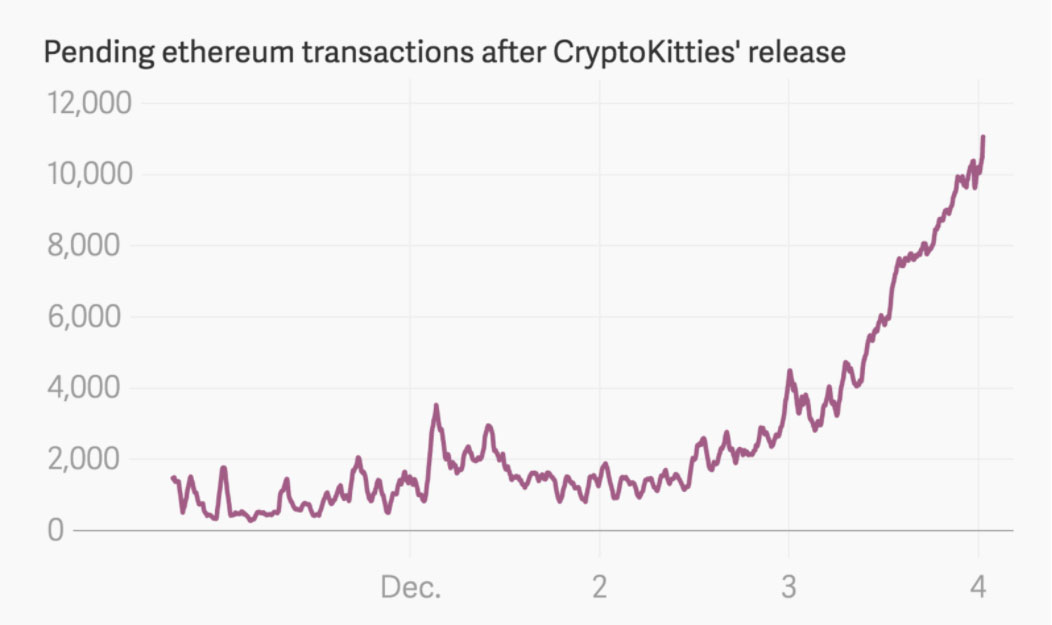

Ethereum became the blockchain of choice for NFT due to the cryptocurrency’s direct support for token creation and storage—no third-party software was required. Later that same year, CryptoKitties emerged, also using the Ethereum blockchain. Purchases of the collectible cats became so frequent (Figure 2) that the transactions caused the Ethereum network to experience substantial lag in December 2017. The average value of each cat is now $65k, some reaching $300k.

Figure 2: The purchase of NFT “Cryptokitties” popularized Ethereum. It is now the second-most used form of cryptocurrency to Bitcoin. (Graph provided courtesy of Medium.)

In 2020-21, NFTs experienced another surge in popularity, including NyanCat (near $600k USD), The CEO of Twitter’s first Tweet ($2.5 million USD), and NBA highlights (collectively grossing over $230 million).

Conclusion:

Crypto is a decentralized form of currency recorded in a digital ledger, commonly known as a blockchain. Like a conventional ledger, this blockchain is a record of each transaction. Because each transaction is unique, it can be assigned a token. These tokens are known as NFTs, distributed as images, audio recordings, or videos. Tiny PNG images of colorful zombies, cats, and LeBron James now have the potential to individually reach values up to $69 million USD—and counting.

Cryptocurrency is often open source. Ethereum has a public white paper, just as Bitcoin does. Source code for the first smart contracts (software that manages transactions) is also free and open software hosted on OpenZeppelin.

As Rozilyn and I researched the timeline of cryptocurrency, questions emerged regarding its diverse and sometimes ideologically conflicting uses. Technology is a tool, and its impacts are often determined by the user. Though Bitcoin was released in 2008, cryptocurrency had existed 20 years prior, and now conceptually for nearly 40 years – its source code shared by enthusiasts around the world. While the use of cryptocurrency has evolved from a shield from predatory mortgage loans to the auctioning of 69 million USD digital cats, the underlying concept of a decentralized currency which is controlled not by institutions, but by users, remains constant.

The artistic and technical experiments detailed in the postings that will follow are intended not to be a serious undertaking by Linux Professional Institute (LPI), but rather, a learning opportunity to involve students in FOSS. But, after all—there’s no harm in a project that “at worst” encourages young professionals to explore open source, and at “best” will support the origin movement of its code by fundraising for open source companies, such as Linux Professional Institute, and the dedicated community members it strives to support.

Rozilyn Marco and Alexander Lamberton are young members of the FOSS community spending their summer internship learning from the Linux Professional Institute (LPI) team. Rozilyn is a third year Electrical and Computer Engineering student at the University of Toronto.

Rozilyn is a committed volunteer of the ON Canada project, disseminating crucial information on the COVID-19 crisis.

Alex is a second year Public Relations student at Algonquin College. Before assisting in LPI marketing, Alex worked in Technology sales, encouraging consumer literacy in basic computer hardware.

Rozilyn creates the software for LPI NFT smart contracts and test ethereum, while Alex designs the ‘human-readable’ NFT code: visuals and written explanations. Both collaborate on research writing blogs, ideas for Tux, and squinting at suggestions on StackOverflow.